This post, another in the “Basics” series, is designed to fill in some of the gaps that can exist for new employees in school finance. I remember when I first started at a school district and was confused by the fact that the attendance data used in Lottery revenue calculations seemed to bear no resemblance to actual ADA. Also, the year-end fourth quarter accrual calculation was not clear. While these things are not too complicated to figure out, surely a universal worksheet could be developed. Well, tada!

REVENUE

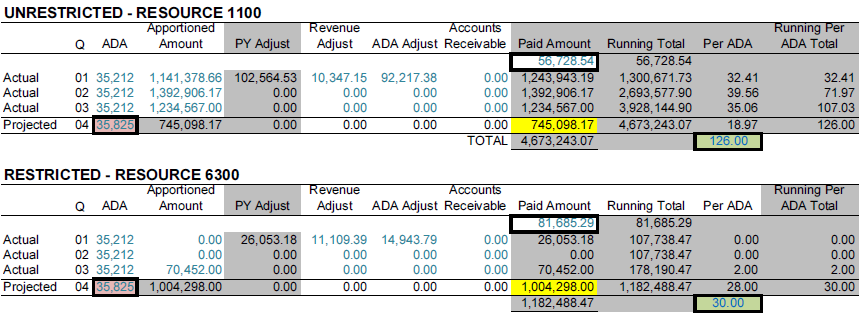

In general, it is helpful to develop projection worksheets that mimic the worksheet you’ll later obtain from the state website. This makes it easier to compare your projections to actual results. And that’s why my Lottery revenue worksheet looks like the State Controller’s schedule.

This worksheet is available for download here.

There are three components to the Lottery revenue calculation:

- Amount per ADA

- ADA

- ADA adjustments

Amount per ADA

Use estimates for budgeting. The fourth quarter lottery payment (accrued in June and paid in September) is still not the final amount, but it is close. Use the numbers issued by School Services of California or/and the CDE . To validate your accrual amount, auditors will want to verify that you used estimates that can be backed up. Usually the letter that is posted to the CDE web site in June is used.

The final actual amount per ADA is determined when the next year’s first quarter payment is made in December. Each year, the California State Lottery withholds a portion of its revenues until after the audit of its year-end financial statements The adjustment that is made the following December will be booked as revenue in that year. This adjustment is minimal – cents per ADA.

ADA

The calculation uses annual Average Daily Attendance. You will be paid on prior year counts all the way through the fourth quarter. You’ll receive a prior year ADA adjustment with the next year’s first quarter payment in the following December. If your ADA is declining, this adjustment will be negative and depending on the rate of decline it can be significant. Since you know your annual ADA when closing the books it is a good idea to anticipate the adjustment and book it in the year it belongs. If you do this you’ll find your fourth quarter payment is “off” from your set-up. It is not until December, when you are paid for the first quarter of the new school year, that will you see your expected prior year ADA adjustment. In my experience most school finance staff do not anticipate this adjustment and allow it be to recognized in the following year. I recommend booking it in the year it belongs, especially if ADA is declining.

ADA Adjustments

ADA is not quite as straightforward as indicated above. Your annual ADA is adjusted by an unexcused absence factor that is the result of funding changes in 1998-99. The factor is historical and fixed at 1.04446.

Through 2014-15 the calculation includes ADA for classes for adults and regional occupational centers and programs that was reported for the 2007–08 fiscal year. Unless the law is amended the expiration of the Adult and ROC/P attendance adjustment will disadvantage unified and high school districts.

EXPENDITURES

Spend the unrestricted portion on anything instructional. Some districts spend their unrestricted funds on specified “extras” such as classroom technology, but after the budget woes of the Great Recession, most districts used the funds to merely survive, meaning they spent the funds by coding teacher costs there. Because there are no supplanting restrictions, Lottery funds are generally used to fund base priorities. Developing a separate plan for Lottery funds is in most cases unnecessary effort. During the year end close, transfer enough teacher costs to the lottery funding to spend it down to zero.

For the restricted portion I have seen some districts allocate some of these funds to sites. I generally do not recommend this, since this brings with it a requirement to monitor site spending to ensure funds are spent only on allowable items. Since the need for instructional materials is high, and the planning and implementation of textbook adoptions is normally done centrally, keep restricted lottery money centrally and spend it on textbook adoptions (before allocating any unrestricted funding to this effort). Since there are no longer any categorical funds devoted to textbooks, that’s the simplest and, I think, the best way to go.